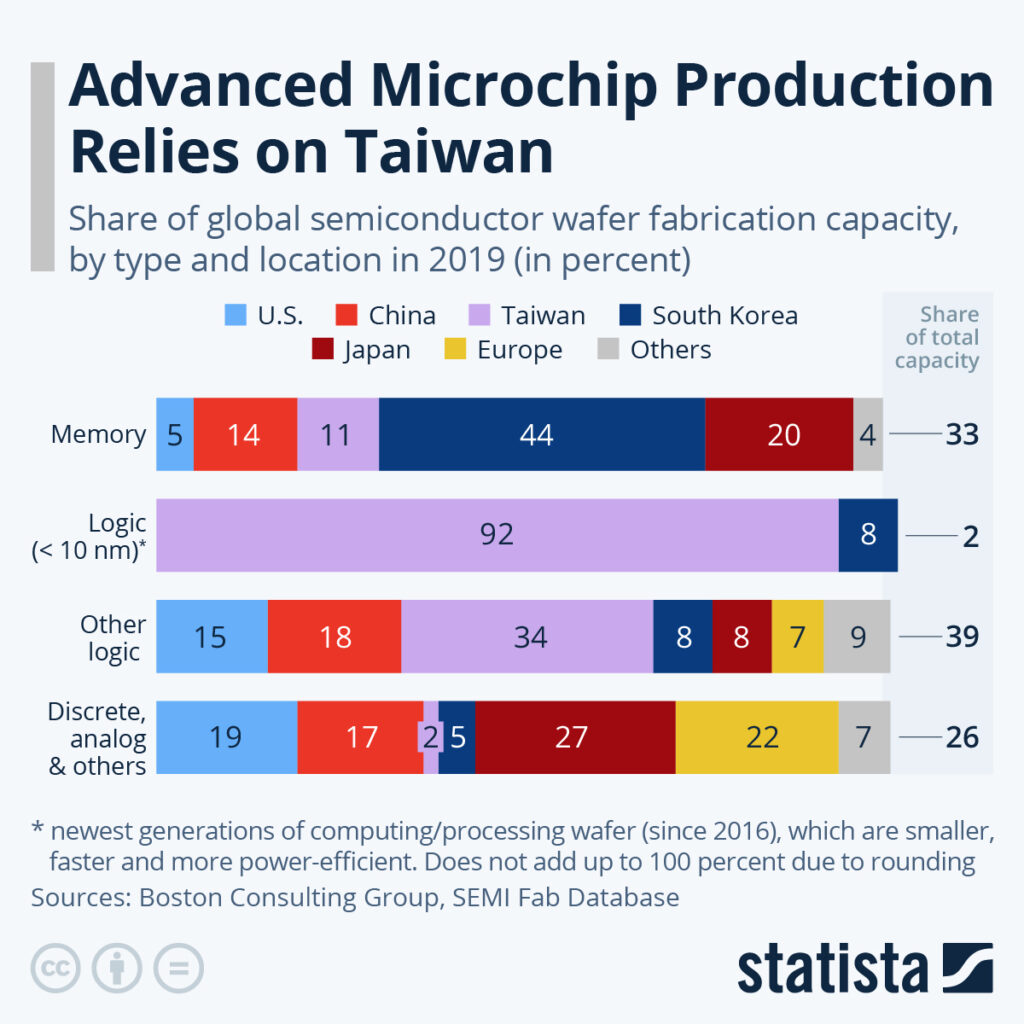

Advanced semiconductor fabrication provides the essential foundation for modern microchip production. Furthermore, these chips power everything from smartphones and computers to medical devices and automotive systems. Because Taiwan produces 92 per cent of logic semiconductors under 10 nanometres, it currently dominates this critical global market.

The Geographic Concentration of Advanced Semiconductor Fabrication

Taiwan and South Korea pioneered the manufacturing processes for chips smaller than 10 nanometres. Specifically, these advanced wafers allow for faster and more energy-efficient processing. Other manufacturing centres did not match this progress initially. Although these advanced chips represented only 2 per cent of global capacity in 2019, experts expect their market share to grow rapidly. Consequently, this technology remains vital for the ongoing innovation in the smartphone and computing sectors.

Historical Shifts in Global Chip Production

The distribution of chip manufacturing has changed significantly over the last three decades. For instance, Europe and the US held a combined global capacity of 36 per cent in 1995. Today, however, that figure sits below 20 per cent. Furthermore, Western nations once controlled over 80 per cent of the market for larger wafer slices in the early 1990s. Because production shifted towards Asia, Western economies now face a long journey to regain their former market standing.

Challenges for Advanced Semiconductor Fabrication in the West

Recent supply chain upheavals and geopolitical tensions highlight the risks of geographic concentration. Therefore, the United States and the European Union have launched major initiatives to challenge the current status quo. Specifically, the US Chips and Science Act aims to encourage domestic manufacturing. However, a significant technological gap still exists. For example, Intel is only now launching its first sub-10 nanometre products. In contrast, the Taiwan Semiconductor Manufacturing Company reached this milestone as early as 2016. Consequently, Western firms must accelerate their development to secure a stable supply of state-of-the-art microchips.

Courtesy: statista.com